How to Buy a Home with lCLT: Affordable Homeownership for Lahaina ‘Ohana

1. Household Income

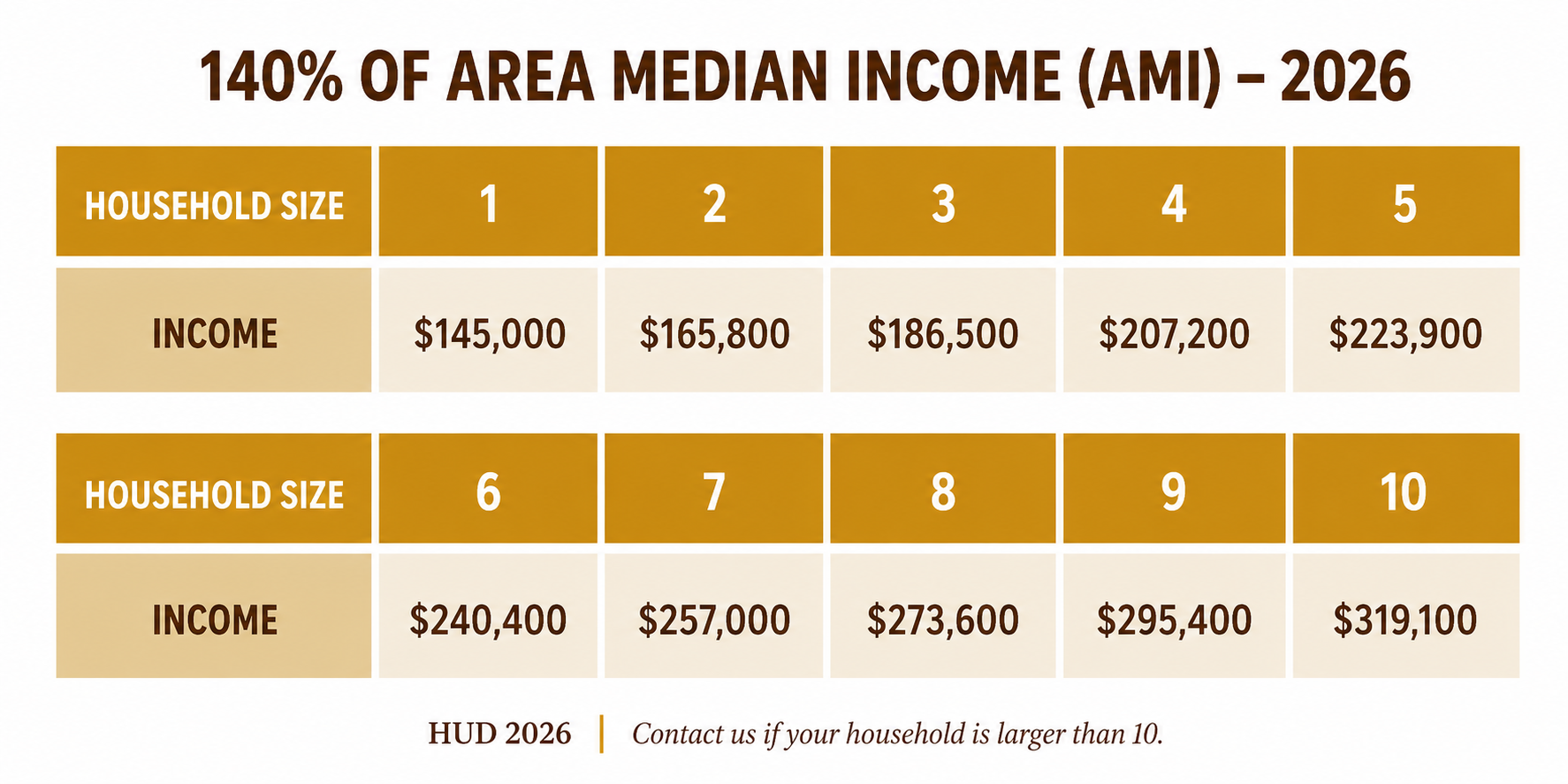

To be eligible to purchase a Lahaina Community Land Trust home your gross household income may not exceed $300,000 or 140% of Area Median Income (see chart below), whichever amount is greater.

Each LCLT home uses different funding sources to make it affordable, therefore there are different income requirements depending on which home you purchase. Income limits include:

2. Connection to Lahaina

At this time, homeownership opportunities are prioritized for households whose homes were damaged or destroyed in the 2023 Lahaina fires and who currently reside on Maui. As the program grows, additional opportunities may become available for other households. We encourage all interested households to complete the Homebuyer Intake Form to stay connected for future opportunities.

3. Household Savings & Assets

Your household must have a minimum of $1,000 in liquid assets to qualify to purchase a LCLT home. Household assets include all checking, savings and investment accounts and do not include IRS designated retirement accounts. Your total non-retirement assets may not exceed $500,000.

Additionally, please note that you cannot buy LCLT home if you have more than a 33% interest in another residential property.

4. Financing Your home

Most buyers will work with a lender to finance their home. While LCLT is not a lender, we partner with trusted organizations who can help guide you through that process. Lenders typically look at a few key things when determining loan eligibility:

Income: You must be able to document adequate, steady household income so that your house payment does not exceed 30% of your gross monthly income.

Credit & Financial History: A credit score of 620 or higher is generally needed to qualify for a mortgage, depending on your lender. If your score is lower, you may still be eligible based on compensating factors. If you do not have a credit score, eligibility may be determined based on documented alternative credit history (such as utility bills, landlord references, etc).

Maximum Debt: Your total debt payments, including your future house payment, should generally be at or below 44% of your gross monthly income, depending on your lender.

If you’re not sure where you fall, that’s completely okay. We’re here to help you understand your options and connect you with the right resources.

Steps to LCLT Homeownership

The steps in LCLT’s home-buying process are designed to ensure we have all the information needed to help you successfully obtain a mortgage and purchase your LCLT home.

The information you share will be kept confidential and used only to support your household and help us determine your eligibility for housing opportunities.

Our process is also designed to ensure you have all the information you need to feel confident if/when you decide to buy a home and understand what is involved. If you have questions, please email us at ComeHome@LahainaCommunityLandTrust.org

Steps to becoming an LCLT homeowner:

Get started: Be ready with your ‘ohana’s information, including household size, household income and non-retirement assets, and the total years lived in the Lahaina area (96761) for the applicant or co-applicant who has lived there the longest. Please ensure all information is accurate and can be verified.

Submit a short intake form: (one per household, please) We use this information to learn about your household and determine your eligibility for future housing opportunities and lotteries. After completing the intake form, check your email and click the verification link to complete your submission.

Join the lottery when homes are available: If a home matches your household’s needs, we’ll invite you by email (and text, if you opted in) to complete a lottery screening form using your unique link. Households who submit the form will be entered into a fair and random lottery conducted by an independent third party.

If selected in the lottery, complete an application: The top 10 households selected through the lottery are prioritized based on years lived in the Lahaina area (96761 zip code) by the applicant or co-applicant who has lived there the longest. If households have the same number of years in Lahaina, priority will follow the original lottery order.

If invited to apply, you will be asked to verify this person’s residency and submit supporting documentation, including financial information. Any misrepresentation or failure to verify information will result in ineligibility.

Being invited to apply does not guarantee a home. Homes are offered to qualified applicants in priority order, and additional applicants may be considered if earlier applicants are not eligible or choose not to move forward.

Secure financing: Complete a homebuyer education course with an LCLT partner, such as Fannie Mae, and work with a lender to understand your options and secure financing for your home.

Purchase your LCLT home!